We are always available and open to answer your questions and concerns. Talk to us, to have a better clarification

Have you ever found yourself relaxing on your bed, catching up on Instagram, and you spot yet another post of someone buying their dream car, booking a vacation to the Maldives, or moving into a new home? Meanwhile, you’re left wondering: Where does all my money go?

It’s a frustrating feeling, isn’t it? Especially when you’ve been saving every rupee—from your piggy bank days to modern savings accounts. So, where did things go wrong? While everyone else seems to be effortlessly growing their money, here you are, working hard but still struggling to make more. The key here is, when it comes to managing your money wisely, the first question you need to ask yourself is: “Where should I save my hard-earned money?”

When it comes to saving your hard-earned money, bank accounts are the most common options that come to mind. They offer safety, liquidity, and modest savings account interest rates. Yet, with inflation climbing faster than ever, relying solely on a bank account could mean your money isn’t working hard enough for you.

Let’s dive deeper. The average savings account interest rate in India hovers around 3-4% per annum. If inflation is at 6%, the purchasing power of your money is actually decreasing over time. Now, what if there was a way for not just savings but also growing your money at a faster pace? That’s where alternative savings options like chit funds come in, offering potentially higher returns while supporting your financial goals.

So, the big question is: Savings account or chit fund—which is the smarter choice for savings and financial growth? Let’s compare these two to find the best fit for your goals.

A savings account is a secure place to park your money while earning a little extra in the form of savings account interest. Banks offer these accounts to help you save systematically while giving you quick access to your funds whenever needed.

The beauty of a bank account lies in its simplicity and accessibility. Here are some standout benefits:

Need cash quickly? A bank account lets you withdraw funds anytime, either through ATMs, online banking, or even a visit to the branch.

With insurance coverage of up to ₹5,00,000 by the Deposit Insurance and Credit Guarantee Corporation (DICGC), your deposits are protected, giving you peace of mind.

Though modest, the savings account interest rates offered by banks ensure your money grows steadily. For instance, many banks offer rates between 3-4% annually.

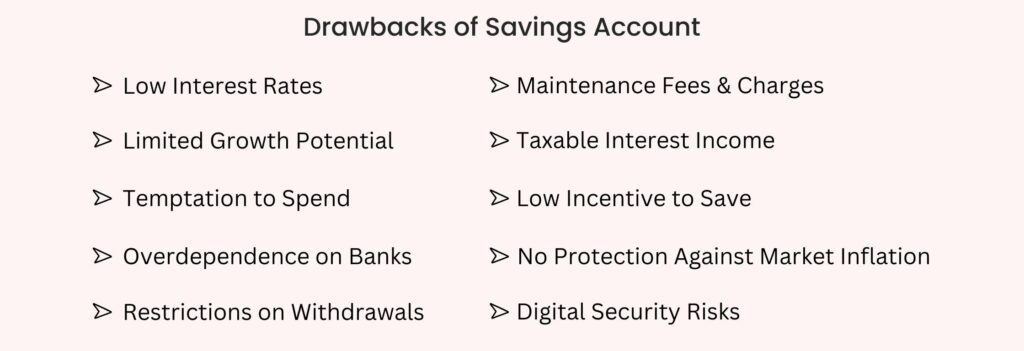

However, let’s be real—bank accounts have their downsides too:

With average savings account interest rates often trailing inflation, your purchasing power might decrease over time.

A bank account is great for short-term investment and savings goals but not for achieving long-term investment goals like retirement or wealth building.

If a bank account is your safety net, a chit fund is like a financial multi-tool offering both the discipline of savings and the flexibility of borrowing when you need it most. The dual nature of these savings plans makes them incredibly versatile.

If you don’t need the money immediately, your monthly contributions build your savings. But if you do, you can borrow the pooled savings amount for your financial needs.

Unlike the modest savings account interest rates, investment pools can offer better value through dividends distributed among members.

Need funds for a medical emergency, a wedding, or a business investment? They provide a hassle-free way to access lump sums without the paperwork of a loan.

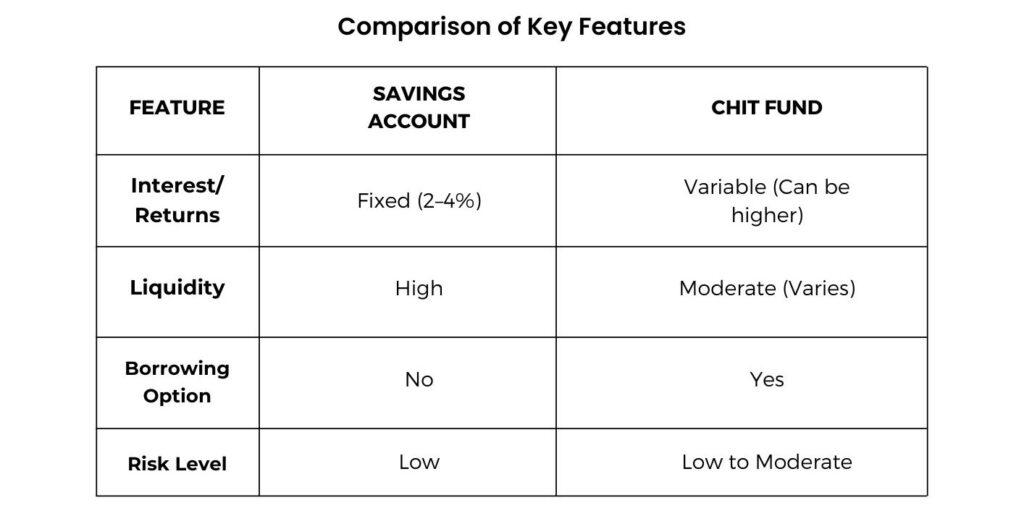

Let’s compare the savings account interest rates (typically 2–4% per annum) with the potential returns offered by chit funds, which often exceed these rates due to dividends.

Imagine that you are depositing ₹10,000 each month into a bank account offering a savings account interest rate of 4% per annum for 10 months. The total balance in the would be approximately ₹1,01,513.41. This includes both the principal amount of ₹1,00,000 and the accrued interest [on the savings] of ₹1,513.41. Which means your profit is ₹1,513.41.

You join a ₹1,00,000 Fixed Dividend Chit Fund scheme with 10 members participating. As it is a fixed dividend chit each member will receive assured dividends and so would pay less than ₹10,000. Here’s how the returns could work:

Investment pools are one of the financial instruments that are designed to offer tangible returns on savings within a shorter period, making them attractive for those seeking immediate financial gains on their savings.

The interest rates of bank accounts often hover between 3–4% annually. Add inflation to the mix, and your “savings” may actually lose value over time. Chit funds, on the other hand, provide dividends, for the savings, that can significantly boost your returns.

Need urgent funds? Bank accounts can limit withdrawals or impose penalties. With chit funds, you can bid for the money you need without restrictions or affecting your savings. Simple, flexible, and penalty-free savings.

Your savings contributions help other members achieve their financial goals, fostering collective savings growth while ensuring your returns on your savings are fixed.

Bank accounts often fall short when it comes to catering to individual savings goals. With fixed interest rates and limited options for customization, they lack the flexibility needed for personalized financial planning. Chit funds, on the other hand, empower you to align your savings strategy with your unique personal finance objectives—whether it’s buying a car, funding your child’s education, or starting a business. This adaptability makes chit funds an excellent choice for those seeking tailored solutions to meet their financial aspirations.

Investment pools are more than just a savings tool—they’re a lifeline for those seeking smarter financial solutions, but they truly shine for:

Running a small bakery and need funds to expand? While a bank account is a safe place to park money, its growth depends on savings account interest rates, which are typically low (around 3-4% annually). Chits, however, provide quick access to lump sums, that is your savings. They provide a structured way to save while offering access to lump-sum amounts through auctions.

Think about the big expenses in life—your child’s education, a wedding, or even a dream vacation. Families often rely on a savings account as their preferred choice. While it’s risk-free, the savings account interest adds up slowly, especially for short-term goals. In contrast, investment pools let you save regularly while offering higher returns and flexibility. Imagine saving ₹5,000 monthly in a chit scheme. By the end of the tenure, you could earn dividends and have access to a lump sum—far outpacing what you’d earn in a savings account.

Saving consistently is tough. But the investment pool makes it almost automatic. Unlike a savings account, where the temptation to withdraw is strong, community funds lock in your contributions, ensuring you stick to your savings plan.

Here’s the truth: Savings accounts are excellent for liquidity, but their growth potential is limited by savings account interest rates, which often fail to beat inflation. The flexible savings plan uniquely blends disciplined savings with the potential for higher returns.

Rotating Savings Schemes often spark curiosity, but let’s face it—there are some misconceptions floating around. Are they safe? Are they transparent? Let’s clear the air and see how regulated community funds stand tall as a reliable savings option.

It’s a common concern, but here’s the truth: regulated funds operate under strict guidelines laid out by the Chit Funds Act, 1982. Companies are legally bound to follow these rules, ensuring transparency and investor safety.

Unlike the unpredictable returns of a savings account tied to fluctuating savings account interest rates, community savings offer a structured system where your contributions are safeguarded by regular audits and government oversight.

These accounts are undoubtedly secure, but their growth is slow, thanks to savings account interest rates averaging just 3-4% annually. Community savings, however, combine disciplined savings with the potential for higher returns through dividends.

Transparency is the backbone of regulated collective savings funds. Regulated companies ensure every participant knows the rules, auction process, and returns in advance. Detailed records are maintained, and every transaction is monitored. A savings account—while safe, many customers are unaware of the impact of savings account interest on long-term growth, often leaving their funds stagnant.

Why let your money sit idle in a bank account earning minimal interest? Take control of your financial future by exploring regulated investment pools. These offer flexibility, higher returns, and the chance to access lump-sum funds when you need them most.

We are always available and open to answer your questions and concerns. Talk to us, to have a better clarification

Corporate Office: RR Tower 3, Water Works Road, SIDCO Industrial Estate, Guindy, Chennai, Tamil Nadu 600 032

Head Office: 1021/2, Vetri Towers, Avinashi Road, Coimbatore -641 018

Call us: +91 844-844-9027

©2026. Kopuram Chits Private Limited, All Rights Reserved.

Powered by Kopuram Chits Private Limited

Fill the Form

We are happy to assist you!