Smart Investment, Secure Future – Build Wealth with Confidence!

Investment plays a crucial role in ensuring financial stability, achieving life goals, and protecting wealth from inflation and unexpected financial challenges.

What is investment?

Investment is the process of allocating money, time, or resources into assets or ventures with the expectation of generating a return or profit in the future. It involves putting funds into financial instruments, businesses, or tangible assets to grow wealth over time.

Investment Strategies

Involves holding investments for several years to benefit from compounding and capital appreciation

- Seeks to grow wealth through the power of compounding by holding investments over the long term.

- Less concern about short-term market fluctuations.

- High risk due to unpredictability of outcomes.

Capitalizes on short term market fluctuations.

- Involves active trading.

- Requires close market monitoring.

- Day trading or swing trading.

Involves disciplined research and patience to identify undervalued assets and benefit from long-term capital appreciation.

- Focuses on companies with good earnings potential.

- Looks for stocks with low price-to-earnings ratios.

- Targets stocks that have temporarily fallen out of favor.

Focuses on identifying and investing in companies that are expected to outperform their industry or the overall market.

- Emphasizes revenue and earnings growth as key indicators of potential success.

- Involves investing in technology or innovative companies.

- High-risk, high-reward investment.

Emphasizes generating a steady stream of income through dividends or interest payments.

- Common investment vehicles often include dividend-paying stocks, bonds, or real estate.

- Suitable for retirees or those seeking regular income.

Tracks a specific market index (e.g., S&P 500, Nasdaq Composite)

- Lower fees compared to actively managed funds.

- Broad market exposure and diversification.

- Suitable for long-term investors.

Focuses on investing a fixed amount of money at regular intervals, regardless of market conditions.

- Involves gradually accumulating shares of an investment over time to smooth out the average purchase price.

- Encourages consistent investing habits.

Involves actively adjusting the mix of assets in a portfolio based on changing market conditions and economic forecasts.

- Combines elements of both strategic & active investing.

- Entails rebalancing the portfolio between stocks, bonds, and cash based on short-term market predictions.

Involves capitalizing on the performance of specific sectors during various phases of the economic cycle.

- Needs careful analysis of the performance of different sectors during each phase of the economic cycle to identify potential opportunities and risks.

- Carries higher risk than a buy-and-hold strategy.

- Involves frequent trading and the potential for mistiming market movements.

Includes non-traditional asset classes like real estate, hedge funds, private equity, & commodities.

- Diversifies a portfolio beyond stocks and bonds.

- Diverse investment opportunities with different risk-return characteristics.

Why Investment is a Smart Choice for Financial Growth

Invest Today, Enjoy Tomorrow: The Benefits of Smart Investing

Achieving Financial Goals

Invest strategically to reach major financial milestones, whether you aim to buy a home, fund your children’s education, or secure a comfortable retirement.

Wealth Accumulation

Investing can be a great way to accumulate wealth over time, especially when combined with consistent contributions and strategic planning.

Financial Independence

Get financial freedom with passive income from your investments. Make your first bold move toward a secure and prosperous future by starting to invest early. After making your decision, you proceed to purchase the asset.

Hedge Against Inflation

Inflation chips away at your money's purchasing power. Smart investment can help your money grow at a faster rate than inflation, preserving its value.

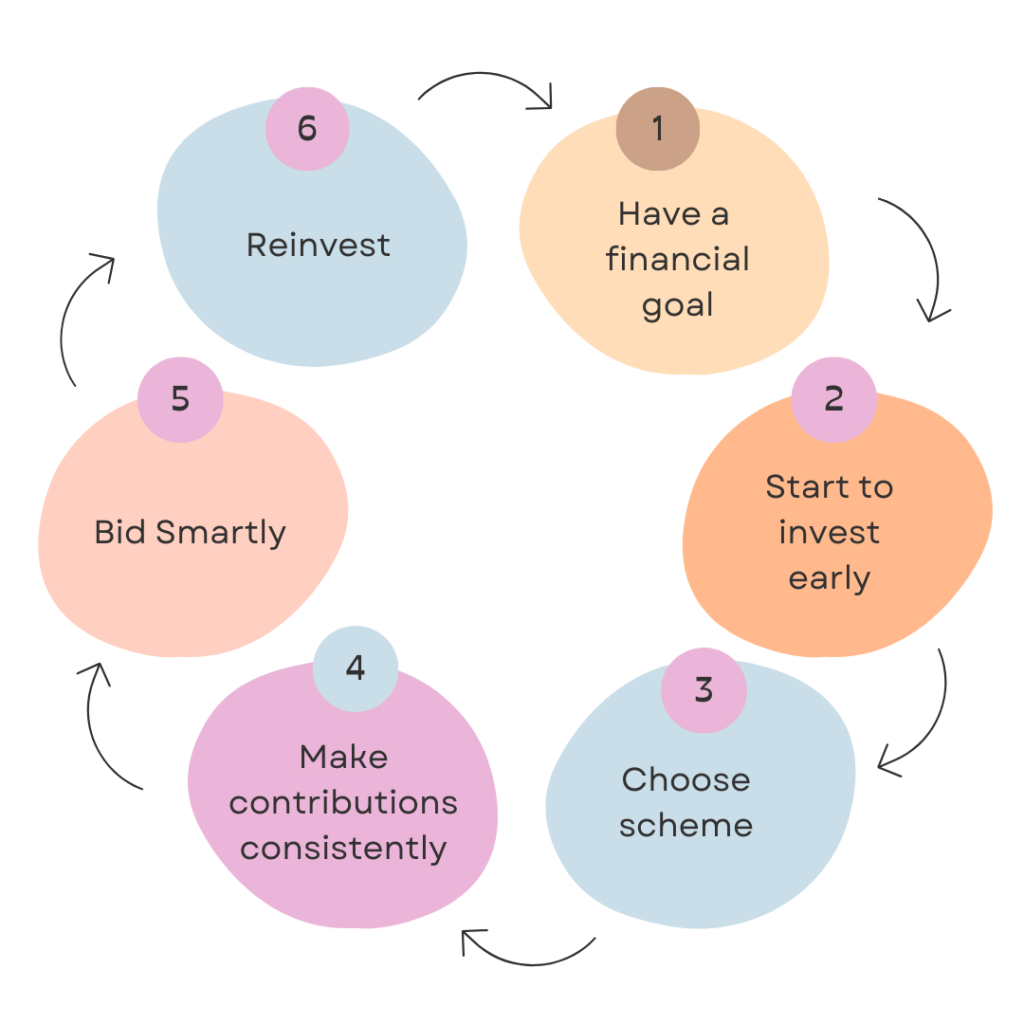

How Investing Works: A Guide to Wealth Building and Financial Security

Choose Your Investments

You start by selecting the type of asset you want to invest in, such as stocks, bonds, real estate, or mutual funds. All types of investments have different risk levels and potential returns.

Purchase the Asset

Once you’ve decided, you buy the asset. For example, if you invest in stocks, you purchase shares of a company. If you invest in real estate, you might buy a property.

Hold and Manage

After purchasing, you hold onto your investments. During this time, the asset may appreciate in value, generate income (like dividends or rent), or both. It’s important to monitor your investments and market conditions to make informed decisions.

Compound Growth

Over time, your investments can grow through compounding. This means that not only do your initial investments increase in value, but the returns you earn can also generate further returns.

Sell or Redeem

When you decide to sell your investments, you can realize any gains or losses. The objective is to sell at a price higher than what you originally paid, thereby realizing a profit.

Reinvest or Diversify

After selling, you can reinvest your profits into other assets or diversify your portfolio to spread risk and enhance potential returns.

Explore Your Investment Options

Explore various investment opportunities. Investment bankers can guide you with valuable insights to help you make smarter financial decisions, aligned with your goals.

Stocks (Equities)

Stocks represent ownership in a company, and when you purchase them, you become a shareholder, owning a portion of that company. The value of your investments rises and falls based on the company’s performance and broader market conditions. Stocks tend to be riskier than other forms of investments because their prices can be highly volatile, meaning they can rise or fall sharply in response to news, earnings reports, or economic shifts. However, over the long term, stocks have historically offered higher returns than most other types of investments. Additionally, some companies pay dividends, which provide a regular income stream on top of potential stock price appreciation.

Bonds

Bonds are investments that are like loans that you give to a company or government for a period of time. When you buy a bond, you’re essentially lending money to the issuer, which could be a government, municipality, or corporation. In return, the issuer promises to pay you a specified interest rate during the life of the bond and to repay the principal amount (the face value) at maturity. Bonds are considered safer than stocks because they offer more predictable returns and are less volatile. However, they generally offer lower returns. Bonds are often used to balance risk in a portfolio, providing steady income while reducing exposure to stock market volatility.

Mutual Funds

A mutual fund is like a basket of investments bought with money from many people. This diversification helps spread risk, as your investments are distributed across a range of assets, rather than relying on the performance of a single stock or bond. Mutual fund investment is a great option for those who don’t have the time or expertise to pick individual investments, as the fund manager makes decisions on behalf of the investors. The downside of this investment strategy is that mutual funds often come with management fees and expenses, which can eat into your returns over time. However, they are widely regarded as balanced and relatively safe investments.

Real Estate

Investing in real estate involves purchasing property such as land, residential homes, or commercial buildings with the intent of generating income through rent or capital appreciation. Real estate can provide stable, long-term returns and can be less volatile than stocks, especially if you hold the property for several years. However, real estate investments require significant capital upfront, and managing property can be time-consuming. Additionally, the value of real estate can be influenced by market conditions, interest rates, and location-specific factors.

Exchange-Traded Funds (ETFs)

ETFs are akin to mutual funds but are traded on stock exchanges like individual stocks. They provide diversification by holding a variety of assets such as stocks, bonds, or commodities. ETFs are popular because they offer flexibility, allowing investors to buy and sell throughout the trading day, unlike mutual funds, which are priced only at the end of the day. They typically have lower fees compared to mutual funds and offer a simple way to gain exposure to broad market indexes or specific sectors. However, since ETFs track market indexes, their performance is tied to the general market’s ups and downs, making them subject to market risks.

Fixed Deposits (FD’s)

Fixed deposits (FD’s) are low-risk investments where you deposit a lump sum of money with a bank or financial institution for a fixed period, earning a guaranteed interest rate. FD’s are highly secure, as they are backed by the government in many countries, and they offer a stable return, making them ideal for conservative investors or those looking for a safe place to park their money. The downside is that the returns on FD’s are generally lower than those of other best investment plans like stocks or mutual funds, and your money is locked in for the duration of the deposit, limiting liquidity. FD’s are often used by risk-averse investors as part of a diversified portfolio.

Recurring Deposits (RD’s)

Recurring Deposit (RD) are types of investments where you can deposit a fixed amount of money every month into an account for a predetermined tenure, typically offered by banks. Unlike Fixed Deposits (FD’s), where you deposit a lump sum, RD’s allow you to save in smaller, regular installments. The interest on RD’s is fixed at the time of account opening and is compounded periodically, providing guaranteed returns at maturity. RD’s are ideal for individuals who want a disciplined, low-risk saving option without locking in a large amount of money at once. The main advantage of RD’s is the assured return, as the interest rate is not subject to market fluctuations, making them a preferred choice for risk-averse investors. However, the returns are generally lower compared to market-linked investments, and withdrawing before maturity may incur penalties.

Systematic Investment Plan (SIP)

A Systematic Investment Plan (SIP) is a method of investing in mutual funds where you can contribute a fixed amount regularly—usually monthly—into a chosen mutual fund scheme. SIP investments make investing in the stock market more manageable by allowing you to invest small sums over time, instead of making a large one-time investment. SIPs benefit from rupee cost averaging, meaning you buy more units when prices are low and fewer units when prices are high, thus averaging out the cost. SIP investments also leverage the power of compounding, where your returns generate their own returns over time, making them a great option for long-term wealth creation. While SIPs come with market risks (as the returns depend on the performance of the mutual fund), they offer higher potential returns than fixed-income instruments like RD’s or FD’s. SIP investment plans are perfect for investors seeking a structured, long-term strategy to grow wealth while gaining exposure to equity markets.

Chit Fund

Chit funds are unique investment options popular in India, where a group of individuals contributes a fixed amount regularly, pooling the funds for members to access as needed. This system encourages disciplined savings while allowing participants to obtain a lump sum for significant expenses like purchasing a home or funding education. Chit funds offer a unique blend of community, flexibility, and financial benefits. While chit funds can offer potentially higher returns through surplus sharing, they come with risks such as default risk. Overall, chit funds can be beneficial for those seeking a structured saving approach, but it’s essential to choose reputable companies and assess individual financial goals and risk tolerance.

Investment Styles

Active Investing

- Involves actively selecting and managing individual securities.

- Seeks to beat the market by pinpointing undervalued stocks or funds.

- Requires extensive research, analysis, and time commitment.

- Typically comes with higher fees due to active management.

- Can be suitable for investors with a high risk tolerance and the ability to dedicate time and resources to research.

Passive Investing

- Involves investing in index funds or exchange-traded funds (ETFs) that track a specific market index.

- Aims to match the market’s performance without attempting to outperform it.

- Requires less research and time commitment.

- Usually carries lower fees due to passive management.

- Can be suitable for investors who prefer a hands-off approach and are comfortable with market returns.

Investments vs. Speculations

- Investments involve putting your money into assets with the expectation of generating steady growth or income over a long period. The goal of investing is to grow wealth over time while preserving the principal. Secure Investments tend to be long-term, focused on gradual wealth accumulation, and often backed by strong data and analysis.

- Speculation, on the other hand, involves taking higher risks in the hope of making quick, large gains. Speculators are often less concerned with the intrinsic value of the asset and more focused on short-term price movements. This approach is more about predicting market fluctuations or capitalizing on trends without the same level of detailed analysis or security. Speculation can involve assets like cryptocurrencies, penny stocks, or commodities, where prices can change dramatically in a short time.

How Investment Helps Grow Your Money & Build Long-Term Wealth

Compounding

When you invest, any returns you earn can be reinvested, which allows your initial investments to grow exponentially over time. For example, if you invest in a mutual fund that pays dividends or interest, those earnings can be reinvested to generate even more returns. Over the years, this snowball effect helps grow your wealth significantly.

Capital Appreciation

The value of your investments can increase over time. For instance, if you buy stocks in a company and its business grows, the stock price is likely to rise, allowing you to sell it later at a profit. Similarly, real estate values may appreciate over time, giving you higher returns when you sell the property.

Income Generation

Some investments provide regular income in the form of interest, dividends, or rent. Bonds, for example, pay interest over time, while stocks can pay dividends. This income can either supplement your current earnings or be reinvested to further grow your wealth.

Common Investment Mistakes To Avoid

- Lack of Research – Investing without understanding the asset, market trends, or risks involved.

- Not Diversifying – Putting all money into a single asset or sector, increasing risk exposure.

- Emotional Investing – Making impulsive decisions based on fear or greed instead of logic.

- Ignoring Risk Assessment – Not evaluating the risk level of an investment before committing funds.

- Timing the Market – Trying to predict market highs and lows instead of focusing on long-term growth.

- Overlooking Inflation – Choosing low-return investments that don’t outpace inflation, reducing purchasing power.

- High-Fee Investments – Investing in options with excessive fees that eat into returns.

- Ignoring Tax Implications – Not considering how taxes impact investment profits.

- Not Reviewing Portfolio Regularly – Failing to rebalance or adjust investments based on market changes.

- Investing Without a Plan – Not setting clear financial goals or investment strategies.

Why Chit Funds Are the Smartest Investment Choice

5 Reasons to Choose Chit Funds for Your Investment

Chit funds allow you to access large sums when needed. Ideal for short and long term financial goals.

You can save regularly while having the option to borrow from the pool.

With risk distributed across all members, chit funds provide a safer alternative to market-dependent investments like stocks.

Chit funds often yield better returns than traditional options like fixed deposits, helping you grow your wealth faster.

Unlike stocks or mutual funds, chit funds aren’t affected by market volatility, offering more predictable returns.

Supercharge Your Investment Goals with Chit Funds

Savings

Build a strong financial foundation for a comfortable life.

Child Education

Build a fund for your children’s education, ensuring they have access to quality education.

Marriage

Plan for your dream wedding without the burden of debt.

Medical Expenses

Cover medical costs without impacting your financial stability.

Retirement

Save for a comfortable retirement and a secure and stable future.

Business Expansion

Secure capital for starting or expanding a business.

Purchasing Car

Save enough for a down payment or purchase your dream car outright.

Dream House

Save and accumulate funds for a down payment or purchase of your dream home.

Debt Repayment

Access funds to pay off high interest loans or credit card debt.

Emergency Fund

Prepare for life's surprises with a financial cushion.

Travel

Accumulate funds to enjoy vacations or special experiences.

Chit Fund Investment: A Smart Way to Grow Your Wealth and Secure Your Finances

Zero Risk, Maximum Reward!

Since contributions come from multiple participants, the impact of any individual default is minimized.

With regular contributions, members build their savings systematically. Reduces the likelihood of impulsive spending. Cultivates disciplined savings habits.

Get returns that are generally higher than market-driven investments. Stop worrying about market conditions.

Know where your investments are going and how they are managed. Get detailed records of contributions and payouts.

Enhanced compliance and thorough audits ensure transparency, accountability, and prevent fraudulent activities.

Access funds when needed and manage financial emergencies effectively, without the stress of market fluctuations.

Empower Your Investments With Assured Returns

Unlike market-based investments, where returns fluctuate based on external factors, chit funds give you assured returns either through bidding or as a lump sum.

No Market-linked Loss

Market volatility is not a concern. Your principal is safe.

Stable Growth

The dividends you earn from chit participation increase your financial growth.

Emergency Bid

You can make an emergency bid and get the money when you need.

Extra Benefits

Get bonuses to boost your overall wealth.

Tax Benefits

Get tax benefits on your dividends to gain most out of your investment.

Why Choose Kopuram Chits for a Reliable Investment Opportunity?

Build Wealth

Achieve your financial goals with consistent savings.

One-Touch Cash

Access funds instantly with just a click.

#KASH

Join, pay, and withdraw money on the go.

Tax Benefits

Enjoy tax-free dividends.

No Collateral Required

No assets needed to start.

Easy Liquidity

Get your funds when you need them.

Investment Flexibility

Save daily, weekly, or monthly—your choice.

High Returns

Benefit from competitive rates and higher returns than traditional banking products.

Financial Security

Invest with a registered company and enjoy peace of mind.

Multiple Schemes

Choose a scheme that suits your needs.

Convenient Payments

Pay at your convenience—online, in-person, or through our agents.

Go Digital

Manage your investments effortlessly online.

Loyalty Rewards

Earn bonuses with any scheme you choose.

Easy Bidding

Bid conveniently from the comfort of your home or anywhere.

Quick Enrollment

Join any scheme with just a few clicks.

No Paperwork

Enjoy hassle-free investing.

Guaranteed Returns

Enjoy assured returns on your investments.

Customer Support

Our dedicated team is here to assist you from onboarding.

Join Online in 3 simple steps for a Hassle-Free Investment

Fill Form

Make Payment

You’re now a Subscriber

How to Maximize Your Investment Returns With Chit funds

Turn your aspirations into achievements with every investment.

Frequently Asked Questions (FAQ)

Investment risk is the possibility that an investment’s actual return will differ from its expected return, including the potential for losing some or all of the initial investment.

Inflation erodes the purchasing power of money, so your investments should ideally outpace inflation.

You can begin investing with relatively small amounts, especially with options like fractional shares or mutual funds.

An investment plan should align with your financial goals, risk tolerance, and time horizon.

Start by setting financial goals, assessing risk tolerance, and choosing the right investment option that suits your needs.

Regular reviews are essential, but avoid making impulsive decisions based on short-term market fluctuations.

If you’re unsure about investment strategies or complex financial situations, consulting a qualified financial advisor is recommended.

Kopuram offers transparency, assured returns, and hassle-free online investment plans.

Kopuram ensures reliable investment opportunities with a secure and customer-friendly process.

By selecting the right chit plan, making timely contributions, and reinvesting wisely, you can maximize returns.