We are always available and open to answer your questions and concerns. Talk to us, to have a better clarification

Life in today’s world is very different. High-paying jobs, fancy gadgets, and exotic vacations seem to define success. Designer wardrobes, weekend getaways, and fine dining have become symbols of achievement. Yet, amidst all the dazzle and excitement, an important element often fades into the background: saving. Saving isn’t just about building wealth—it’s about safeguarding your future, turning your dreams into reality, and enjoying the peace of mind that comes with financial security.

That being said, selecting the right investment option is essential. Investing your savings wisely ensures that your savings grow and work for you. It also depends on your financial goals, risk tolerance, and the returns you expect. Postal savings have long been a popular savings avenue for people who value safety and steady returns. They are particularly suited for conservative investors aiming for guaranteed returns for their savings.

But how do their interest rates stack up against other investment options like chit funds? Chit funds? Yes, chit funds! Why not stocks, mutual funds, or cryptocurrencies like Bitcoin? Because here, we’re focusing on investment options that provide assured returns—the kind of returns that are unaffected by market volatility.

Let’s delve into how these options compare, especially in terms of interest rates, safety, and accessibility.

Postal savings offer a fixed interest rate, which is typically lower than other investment options. While they are secure and backed by the government, the low interest rates can erode the purchasing power of your savings over time. Here’s what makes them attractive:

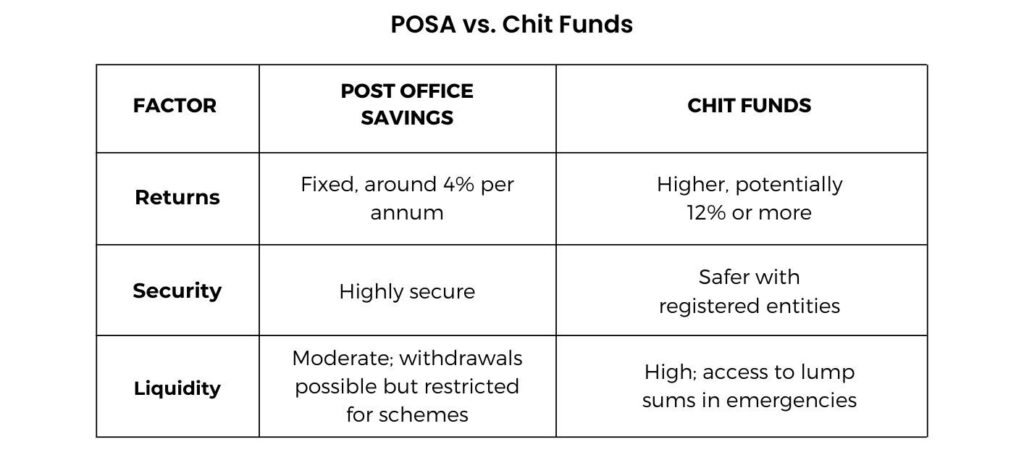

A post office savings account interest rate is generally about 4% per year. While this may not be as high as some other investment options, it is stable and reliable. Other postal savings schemes like the Post Office Monthly Income Scheme (MIS) or Fixed Deposits offer higher returns, often ranging from 6% to 8% per annum, depending on the tenure.

Post office savings accounts are among the safest investment options, as they are fully backed by the government. The likelihood of losing your savings is virtually zero. Unlike other investments that can fluctuate with the market, your principal is guaranteed by the government. This makes it a great option for risk-averse investors or those just looking to park their money somewhere safe.

These accounts are accessible even in rural areas, ensuring that people from all walks of life can save systematically.

Certain post office savings schemes offer tax benefits under Section 80C of the Income Tax Act. For example, if you’re investing in a 5-year Post Office Time Deposit or the National Savings Certificate (NSC), you can get tax relief.

If you’re someone who values predictability, the post office savings account interest rate is a huge advantage. At present, the interest rate is approximately 4% per year. While this might not seem high compared to some other investments, the steady, fixed returns can provide a sense of financial security. Plus, there’s no risk of losing your savings due to market fluctuations.

While you can withdraw savings if you need immediate access to your funds, you may find it less convenient than other options. Additionally, certain post office schemes have a minimum lock-in period, which means you can’t access your savings for a set time.

The returns from post office savings are relatively stable, but they might not keep up with inflation. With inflation rates sometimes running higher than the 4% annual return, you could find that the value of your savings isn’t growing in real terms. This is especially a concern in times when inflation rises faster than the interest rates offered.

More informal and flexible, this savings scheme has the potential for both regular savings and access to lump sums. Members also have the option to bid for the pooled savings.

They can offer higher returns than postal savings, with some savings plans potentially yielding 12% or more.

One of the main benefits is that you can receive a lump sum amount before the end of the saving period. This is especially helpful in emergencies when you need immediate access to funds, without having to wait until the end of the entire term.

Pooled savings allow flexibility in terms of contribution amounts and frequency. You can choose how much you want to contribute, based on your financial capacity, and contribute either monthly, bi-monthly, or weekly depending on the scheme.

It fosters a sense of solidarity and trust among participants, as you are saving with a group of people, some of whom may be family, friends, or neighbors.

For individuals who may not have easy access to formal credit sources or loans, community savings provide an alternative source of credit.

Collective savings plans can serve as a tool for achieving specific financial goals, such as funding a wedding, a child’s education, buying property, or starting a business.

There is a possibility of fraud or default, especially if the savings scheme is not run by a registered company or institution. But if you choose a registered company you need not worry about such risk factors.

If you’re aiming for growth, community savings might be a better choice as they often deliver higher returns—sometimes exceeding 12%—far more attractive than the typical 4% post office savings account interest rate.

Community savings offer a more adaptable savings approach, allowing you to adjust your contributions based on your financial situation. In contrast, postal savings require fixed deposits on a regular schedule to maximize benefits.

Collective savings schemes provide greater flexibility if you need access to your savings unexpectedly. You can bid for and access the savings amount before the scheme concludes, often without heavy penalties. On the other hand, postal savings typically involve a lock-in period, restricting access to funds and imposing penalties for early withdrawal.

These savings schemes can help your savings grow faster and better withstand inflation. With their higher potential returns, they offer a buffer against inflation eroding your savings’ real value. In comparison, postal savings, while secure, may not keep pace with rising inflation, potentially reducing the purchasing power of your earnings.

These savings schemes are more advantageous for accessing a significant sum early in case of sudden expenses. Postal savings, however, make early withdrawals challenging and may result in penalties or diminished benefits.

Collective savings schemes stand out as a dynamic and flexible investment option for individuals seeking higher returns, adaptability, and liquidity. They provide growth opportunities that can exceed the rate of inflation. Additionally, their ability to provide early access to a lump sum without substantial penalties makes them a practical choice for managing unforeseen financial needs. While postal savings are secure and reliable, pooled savings can be a better fit for those looking to optimize their savings and achieve financial goals more effectively.

We are always available and open to answer your questions and concerns. Talk to us, to have a better clarification

Corporate Office: RR Tower 3, Water Works Road, SIDCO Industrial Estate, Guindy, Chennai, Tamil Nadu 600 032

Head Office: 1021/2, Vetri Towers, Avinashi Road, Coimbatore -641 018

Call us: +91 844-844-9027

©2026. Kopuram Chits Private Limited, All Rights Reserved.

Powered by Kopuram Chits Private Limited

Fill the Form

We are happy to assist you!