We are always available and open to answer your questions and concerns. Talk to us, to have a better clarification

Do you have a post office savings account? If yes, can that savings cover all your future needs, help you fulfill your dreams, and ensure a comfortable retirement?

Think about it for a moment. These are important questions because most people simply park their money in a postal savings service without realizing the limitations simply because it feels safe. Being government-backed certainly provides peace of mind. But is the savings you’re setting aside today going to hold its value 10, 15, or 20 years from now? With inflation quietly nibbling away at your savings, are you confident it’s enough to keep up? Or are you just sticking to it because it’s familiar?

Let’s be real—your dreams, like buying a home, traveling, or even living stress-free in retirement, deserve more than just safety. They deserve smart savings strategies that help your money grow.

So, if postal savings services aren’t cutting it, what’s the alternative? In today’s fast-changing economy, finding financial solutions that combine higher returns with lower risk is more important than ever. And that’s where chit funds come in as a real game-changer. Unlike postal savings services, where your money just sits there, chit funds combine both saving and borrowing in a way that maximizes your returns.

Post office savings are a favorite among conservative investors. They offer a sense of security backed by the government but their returns on the savings are modest.

For instance, post office savings accounts typically offer an interest rate of around 4% annually. While this is marginally better than keeping your money idle, it’s hardly a wealth generator. Even fixed deposit schemes under the post office umbrella max out at around 7% in interest rates.

In today’s inflationary world, these returns barely keep up with rising costs, leaving your purchasing power stagnant—or worse, diminished.

For example, if you save ₹1,00,000 in a postal savings service, you’ll earn ₹4,000 in interest in one year. But with inflation working against you, that ₹1,00,000 is really only worth around ₹98,000 by the end of the year. Not exactly what you want when it comes to growing your wealth.

If you want a slightly higher return on investment from your postal deposit account, you might consider a recurring deposit (RD). This scheme allows you to make regular monthly deposits, and in return, you earn a fixed interest rate, which currently hovers around 6.5% per annum. Not bad, but again, inflation can still eat into your returns.

Let’s say you invest ₹20,000 every month in a post office RD for a year. At the current interest rate of 6.5%, you’ll accumulate a little over ₹2,40,000 by the end of the year, including your initial deposits and interest. While it’s a better option than a standard postal savings service, the returns are still modest. With inflation steadily reducing the value of money, this might not be enough to meet your financial aspirations in the long run.

Post office fixed deposits (FD’s) offer a slightly higher interest rate, usually ranging from 6% to 7% per annum, depending on the tenure. Like an RD, your money is locked in for a fixed period—typically ranging from 1 to 5 years. While the post office FD offers more stability than an RD or savings account, it still struggles to outpace inflation in a meaningful way.

For example, if you invest ₹1,00,000 in a post office FD at a 7% interest rate for a year, you’ll earn ₹7,000 in interest. While that’s better than postal savings services, it still doesn’t do much to build wealth over the long term when inflation is steadily increasing.

While postal savings services, recurring deposits, and fixed deposits are safe, government-backed options, they have one major limitation: their returns are relatively low and barely keep up with inflation. So, while you’re saving, your money’s real value is actually decreasing over time. The result? Your savings might not be enough to fund your goals, whether it’s buying a house, traveling the world, or securing a comfortable retirement.

Here’s where chit funds come in as a smart alternative to postal deposit accounts. Unlike postal investment accounts, community savings plans are one of the investment options that combine savings with the flexibility to borrow money when needed, all while offering far higher returns.

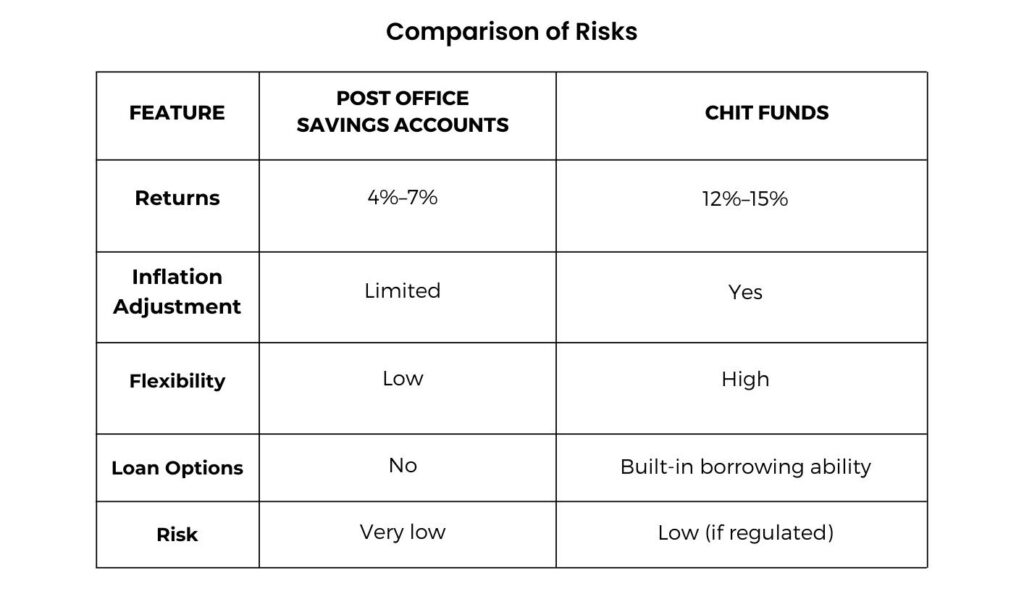

One of the biggest advantages of postal banking service accounts is the returns. The interest rates on community savings can range from 12% to 15% annually, which is a substantial improvement compared to the low returns offered by postal savings schemes, recurring deposits (RD’s), or fixed deposits (FD’s).

For example, if you contribute ₹10,000 a month to this savings scheme, over the course of a year, you could potentially end up with ₹1,50,000—this includes your monthly contributions and the interest earned. Compare that to the ₹1,20,000 you might earn from a post office RD or FD at a 6% interest rate. That’s a difference of ₹30,000, and over time, these gains can significantly add up.

Postal deposit accounts are super safe, no doubt about it. Your savings are backed by the government, the returns are guaranteed, and you don’t have to worry about market ups and downs. Sounds perfect, right?

But here’s the thing— your savings might be safe, sure, but it’s not working hard enough to build wealth. Think of it as parking your car in the garage—it’s secure but not going anywhere.

If you’re looking for absolute safety and don’t mind low returns on your savings, a postal investment account may suffice. But, wouldn’t you prefer your savings to be both safe and growing at the same time while still keeping risk under control? With community savings, you’re not just saving—you’re building a future. They strike a perfect balance between risk and reward, making them a smarter option for growing your savings. Let’s explore why.

While the returns from a postal savings scheme are fixed, community savings often yield higher and assured returns. Chit funds can yield annual returns of 12%–15%, compared to 4%–7% in post office savings schemes. Over 5 years, ₹1 lakh in a chit fund could grow to ₹1.8 lakh, while a post office account may barely reach ₹1.4 lakh.

Another reason community savings stand out is their flexibility. Unlike post office bank accounts, where you can only access your money with a penalty or after a fixed term, community savings allow you to access the pooled money through a bid or auction process. If you need cash urgently, you can participate in the investment pool auction and receive the amount you need, with the remaining balance continuing to grow.

In contrast, if you have a post office savings plan, you would either need to wait for the term to end or pay a penalty for early withdrawal of your savings. This makes community savings a more dynamic option, providing both savings and liquidity when needed.

Just like postal savings schemes, community savings are also a relatively safe option—especially when you choose a registered chit fund with a good track record. These companies operate in a group setting where the participants trust each other, and each member has an equal share of the savings pool. The group dynamic ensures that the savings is being managed responsibly, and unlike bank accounts, you can also know the status of your savings at any time.

Due to the higher returns on savings, chit funds can provide better wealth accumulation over time compared to the low yields on savings from postal financial accounts.

Chit funds offer the ability to access funds quickly and can be a lifesaver in times of need. Ask yourself: if an emergency hits tomorrow, would you rather deal with the paperwork and penalties of a postal deposit account or have the flexibility to access your savings without hassle?

While post office bank accounts only grow your savings, chit funds allow you to access funds when needed without taking out high-interest loans.

With inflation averaging 6%–7% annually, postal savings services barely preserve purchasing power. Chit funds, with higher returns for your savings, ensure real wealth growth.

These investment pools provide not just financial growth but peace of mind—a reliable safety net you can count on. Why not make your savings fund smarter and more accessible?

The social aspect of these savings funds can provide additional value beyond financial returns.

While postal savings are a safe option, community savings scheme funds offer a more rewarding and flexible approach to savings and investment. By understanding the benefits and working with a reputable chit fund company, you can secure a brighter financial future.

So, why settle for less? Explore regulated chit funds today and watch your money grow beyond what postal financial accounts can offer.

We are always available and open to answer your questions and concerns. Talk to us, to have a better clarification

Corporate Office: RR Tower 3, Water Works Road, SIDCO Industrial Estate, Guindy, Chennai, Tamil Nadu 600 032

Head Office: 1021/2, Vetri Towers, Avinashi Road, Coimbatore -641 018

Call us: +91 844-844-9027

©2026. Kopuram Chits Private Limited, All Rights Reserved.

Powered by Kopuram Chits Private Limited

Fill the Form

We are happy to assist you!