We are always available and open to answer your questions and concerns. Talk to us, to have a better clarification

Financial needs are a universal reality, whether you’re an individual or a business. Both individuals and businesses face a variety of financial needs to cover expenses and achieve financial goals. For individuals, financial needs can range from everyday expenses like rent, groceries, and transportation, to larger purchases like cars or homes. You might also need to save for retirement, education, or unexpected emergencies. Businesses, on the other hand, have a whole different set of financial needs. They need money to cover operational costs like salaries, rent, and supplies. They might also need funds to invest in new equipment, expand their operations, or develop new products.

No matter who you are, it’s important to have a solid understanding of your financial needs and develop a plan to meet them. This can involve budgeting, saving, and exploring different financial products like loans or investments.

Chit funds are a traditional savings and borrowing tool popular in India, offering a flexible way to manage money. Participants contribute to a common pool, and one member takes the pot each month—perfect for both saving and borrowing.

Alternatively, many people prefer bank loans. Whether you’re applying for a personal loan, a home loan, or a business loan, banks provide a structured repayment plan with fixed interest rates.

Both chit funds and bank loans have their own advantages depending on your financial needs and situation. If you value flexibility and want to combine savings with borrowing, chit funds might be your best bet. If you prefer a more formal, structured approach, a bank loan could suit you better. As financial tools, they both play important roles in helping individuals and businesses meet their goals. So, how do you decide which option is best for your financial goals? That’s what we’ll explore next—comparing chit funds and bank loans, breaking down their benefits, and limitations, and why chit funds might just be the perfect financial tool for you, to help you make the right choice.

First, let’s take a quick look at what each one is and how they work.

Chit funds are a unique financial tool that combines elements of both saving and borrowing. It’s a concept that’s been around for ages, especially in India. Think of a chit fund as a self-help group for your finances. A group of people contribute a set amount of money into a shared pool every month. The pooled money is then offered to the highest bidder through an auction. The highest bidder gets the entire pot, but they also have to continue contributing to the fund until the end of the cycle.

Chit funds offer a valuable opportunity to:

By contributing regularly, you’re essentially saving.

When you need a loan, you can bid for the auction and potentially get it at a lower interest rate than a traditional bank loan.

The great thing about chit funds is their flexibility and dual-purpose nature. They can be a great way to save money over time, but they also provide immediate access to a lump sum when you need it, without the formalities of traditional loans. If you’re taking the pot early, it’s like a loan because you get money upfront but continue contributing to the pool. If you’re one of the last ones to take the pot, it feels more like a savings and investment plan since you’ve been putting money in every month, and in the end, you get a nice lump sum.

Let’s take an example: Imagine you’re part of a 10-member chit fund group, and each person contributes ₹5,000 a month. This means there’s ₹50,000 pooled together each month. Let’s say you bid in the second month and win the pot for ₹45,000 (you agree to take ₹5,000 less to get the money sooner). You can now use that ₹45,000 for whatever you need, but you still have to keep contributing ₹5,000 every month for the remaining 8 months. Meanwhile, other members benefit from the bonus distribution of that ₹5,000 you gave up.

No financial product is without risk, and it’s important to discuss the risks involved in chit schemes, such as the possibility of default by other members or the potential for fraud in unregulated schemes. However, with proper research and by choosing a reputable chit fund, these risks can be mitigated. All you need to do is look for chit funds that are registered with the Chit Funds Act, 1982, which regulates the industry and provides a legal framework for operations.

The great thing about chit funds is their flexibility and dual-purpose nature. They can be a great way to save money over time, but they also provide immediate access to a lump sum when you need it, without the formalities of traditional loans. If you’re taking the pot early, it’s like a loan because you get money upfront but continue contributing to the pool. If you’re one of the last ones to take the pot, it feels more like a savings and investment plan since you’ve been putting money in every month, and in the end, you get a nice lump sum.

Let’s take an example: Imagine you’re part of a 10-member chit fund group, and each person contributes ₹5,000 a month. This means there’s ₹50,000 pooled together each month. Let’s say you bid in the second month and win the pot for ₹45,000 (you agree to take ₹5,000 less to get the money sooner). You can now use that ₹45,000 for whatever you need, but you still have to keep contributing ₹5,000 every month for the remaining 8 months. Meanwhile, other members benefit from the bonus distribution of that ₹5,000 you gave up.

Bank loans are more structured financial products offered by banks and financial institutions. Whether you’re applying for a personal loan, home loan, or business loan, banks provide a specific amount of money, which you repay over time with interest. The process is usually formal, requiring documentation, credit checks, and collateral in some cases.

Bank loans are suitable for:

When you require a substantial sum to acquire a costly item.

A bank loan can merge multiple debts into one manageable payment.

In case of unexpected expenses, a bank loan can provide a financial cushion.

Now let’s break down the pros and cons of each to help you make an informed choice.

When it comes to borrowing and repayment, chit funds and bank loans each offer different kinds of flexibility. With chit funds, the flexibility comes in how you can use the funds. If you need money urgently, you might be able to get it sooner, depending on your chit fund’s rules. Additionally, the repayment terms are often quite flexible. You’re essentially saving and borrowing simultaneously, so your monthly contributions can be adjusted based on what works best for you and the group.

Chit funds are like a safety net; they offer financial flexibility, unlike the stringent timelines of bank loans - Arvind Mehta, Financial Expert.

On the other hand, bank loans are more structured. When you obtain a bank loan, you are given a one-time amount that you must repay over a specified term, usually through regular monthly installments. However, it can be less flexible if you need to change your payment terms or borrow additional funds. The process is more formal, involving credit checks and detailed documentation.

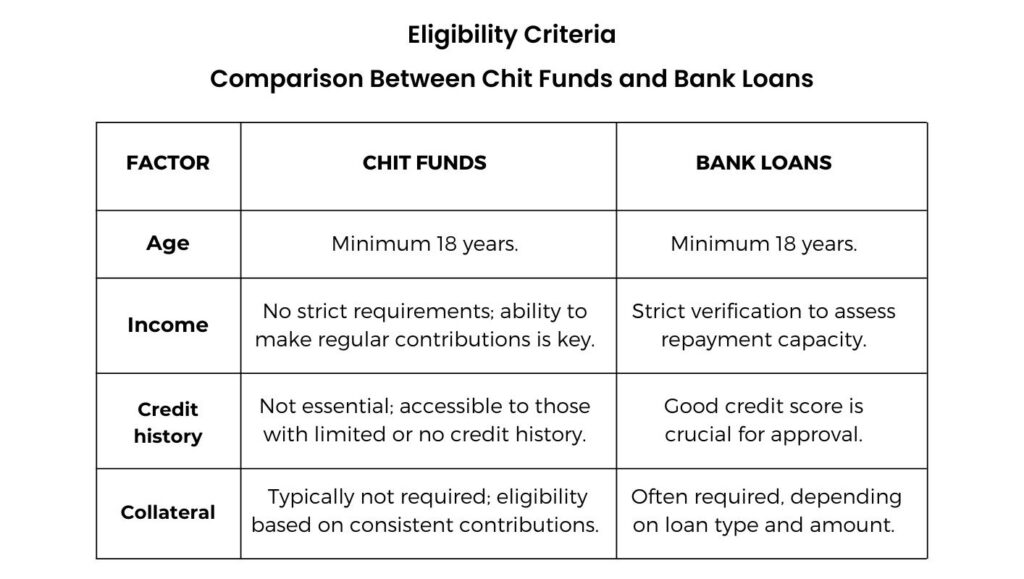

When it comes to accessing financial resources, both chit funds and bank loans have their own eligibility criteria. With chit funds, the process is usually more flexible. All you need is to be a part of a chit fund group and commit to regular contributions. It’s less about credit scores and more about your ability to contribute and participate consistently.

On the other hand, securing a bank loan involves a bit more red tape. Banks will evaluate your creditworthiness, income, and financial history before approving a loan. This often involves stricter requirements and more paperwork.

When it comes to interest rates, chit funds and bank loans operate a bit differently. Bank loans typically have fixed or variable interest rates that can depend on your creditworthiness and the type of loan. These rates can sometimes be on the higher side, especially if your credit score isn’t top-notch.

On the other hand, chit funds don’t always follow the traditional interest rate model. Instead, the returns and contributions are structured around the total amount in the pool and how it’s distributed among members. This can often mean more flexibility and potentially better returns depending on the structure of the chit fund and how well it performs.

Let’s see an example:

For a personal loan (from banks) of ₹5 lakh over 5 years, a 12% interest rate will result in paying around ₹1.7 lakh in interest alone. Yes! You read that right! One of the biggest drawbacks of bank loans is the interest rates, which can range from 10% to 15% (or even higher) depending on the loan type and your credit score.

In chit funds, the interest is often lower compared to personal loans, that is, depending on when you withdraw, the amount paid back might be much less than that.

When it comes to financial flexibility, chit funds stand out as a versatile personal finance option. In comparison, bank loans are often more rigid, designed for specific purposes with strict guidelines on how the funds can be used.

One of the great things about chit funds is how versatile they are in supporting financial planning. Whether you’re saving for an emergency, planning a big purchase, supporting your business, or handling personal expenses, chit funds can adapt to your financial goals. You can use the funds however you like, without any restrictions.

In contrast, bank loans tend to be more rigid. They’re usually designed for specific purposes, like home loans, car loans, or business loans. Each type comes with its own set of rules, and you typically can’t use the money for anything outside that specific purpose. You can use the funds however you like, without any restrictions.

When it comes to getting your hands on the money you need, chit funds and bank loans are pretty different.

With chit funds, once you’re part of a group, the process is generally quick. If you’re the highest bidder at the monthly auction, you can usually receive the funds in just a few days. There’s no lengthy approval process or extensive paperwork involved. There’s no lengthy approval process or piles of paperwork to deal with.

On the flip side, bank loans can be a bit of a waiting game. You’ll need to go through a lot of steps, like filling out applications, submitting documents, undergoing credit checks, and waiting for approval. The bank will then conduct a credit check to assess your creditworthiness. The process may take a few days or up to several weeks.

When it comes to borrowing money, credit scores play a significant role in determining your eligibility for bank loans and the interest rate you’ll be charged. However, chit funds take a different approach.

With chit funds, there are no credit score requirements. You don’t need to worry about your financial history or whether you have a perfect credit rating. As long as you’re part of the chit group and can make regular contributions, you’re eligible. This makes chit funds far more accessible and inclusive, welcoming people from all financial backgrounds.

In contrast, bank loans rely heavily on your credit score. If you’ve got a strong credit score, you’re more likely to get your loan approved with a good interest rate. But if your credit score is low, it can either lead to higher interest rates or even rejection of your loan application altogether.

Chit funds offer a valuable alternative for those who might struggle to meet the credit score requirements for bank loans. They provide a way to borrow money without the strict financial scrutiny that often accompanies traditional lending institutions. This makes chit funds a more inclusive option, especially for people in underserved communities or those who are just starting their financial journey.

Both chit funds and bank loans involve certain risks, but the nature of those risks can differ.

With chit funds, the main risk lies in how the group is managed. If you join a well-established chit group with a good track record, a reputable organizer, and a transparent system you will not face any issues.

On the other hand, bank loans come with their own set of risks, especially if you fall behind on payments. Missing payments can lead to hefty penalties, damage to your credit score, or even loss of collateral, like your home or car if it was secured against the loan.

When it comes to repayment terms, chit funds generally offer more flexibility than bank loans.

Since chit funds are based on group contributions, the pressure to repay is generally lower, especially if you’re participating primarily as a saver. You’re contributing monthly anyway, so there’s less of a structured “payback” feel, and it’s all part of the group dynamic.

Bank loans, on the other hand, have strict repayment terms. You have fixed monthly payments that you must meet, and if you miss a payment, there are usually penalties involved. On top of that, paying off your loan early can sometimes trigger additional fees, known as prepayment penalties.

The best option for you depends on your specific financial needs and circumstances. Here are some factors to consider:

Are you looking for a lump sum for a specific purpose, or do you need a flexible loan option?

Do you have a regular income and can you afford to repay a loan?

Can you get the loan amount quickly?

Can you borrow a specific amount when you need it?

Can you handle the typically higher interest rates that come with bank loans?

Do you have the necessary collateral to secure the loan?

Are you prepared to navigate the lengthy, paperwork-heavy application process?

Are you ready for the potentially long wait during the approval process?

When it comes to managing your finances, both chit funds and bank loans have their merits. However, chit funds really shine when it comes to flexibility, accessibility, and a community-focused approach. They often come with lower interest rates, quicker access to funds, and no stringent credit score requirements, making them a more approachable option for many.

Bank loans certainly have their place but if you’re looking for something that combines the best of saving and borrowing without the hefty interest rates and rigid terms, chit funds are a great alternative. They provide a balanced approach that allows you to save while also giving you the flexibility to borrow when needed.

So, next time you’re weighing your financial options, consider the advantages of chit funds. They could be the versatile, efficient, and financially sound choice that perfectly fits your needs.

We are always available and open to answer your questions and concerns. Talk to us, to have a better clarification

Corporate Office: RR Tower 3, Water Works Road, SIDCO Industrial Estate, Guindy, Chennai, Tamil Nadu 600 032

Head Office: 1021/2, Vetri Towers, Avinashi Road, Coimbatore -641 018

Call us: +91 844-844-9027

©2026. Kopuram Chits Private Limited, All Rights Reserved.

Powered by Kopuram Chits Private Limited

Fill the Form

We are happy to assist you!